Home to five of the top 10 oil producers in the world, the Middle East is well established as a global fossil fuel powerhouse. Indeed it accounts for more than a third of the world’s oil production and almost a quarter of its gas output. Unsurprisingly, countries in the region have been slow to embrace renewable energy – regional share of global capacity stands at 1%, less than half that of Africa.

But even in this fossil fuel stronghold, the clean energy transition is starting to bite. In percentage terms, no other region in the world grew renewable capacity faster last year than the Middle East, not even high-flying Asia (12.8% vs 12%, according to IRENA). And a number of countries have set surprisingly ambitious climate targets:

- The United Arab Emirates (UAE) plans to spend up to $54bn on renewables by 2030 in order to achieve net-zero emissions by 2050.

- Saudi Arabia aims for renewables to account for half its electricity mix by 2030.

- Oman is aiming for 20% renewables by the same date.

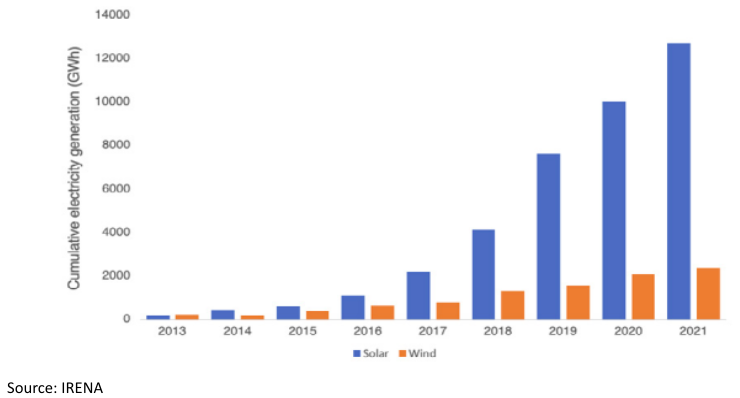

Stellar solar growth

Building out solar power will be key to achieving these targets, and massive strides have been made already. Between 2015 and 2022, installed solar capacity increased 30 times in the region (see chart below) to almost 13,000 GW, compared to less than five times globally. Over the same period, wind capacity grew threefold to 2,400 GW.

Installed wind and solar capacity in the Middle East

With some of the best solar power potential in the world and production growing fast, the Middle East has seen the steepest falls in solar installation costs in the world – in 2022 alone, they fell by 62% in the UAE and by 35% in Saudi Arabia. The UAE’s average installed costs are $578 per kW, half the global average. This means both countries saw the biggest falls in electricity costs, known as the levelised cost of electricity, last year – the UAE’s fell by two thirds and Saudi Arabia’s by almost one third.

Oman sees the lightOman has announced over 18 GW of new solar projects, compared to just 0.3 GW of new oil and gas plants. In 2022, Oman installed more renewable capacity than it had in the previous decade. |

Sovereign wealth funds

The potential to expand renewable capacity faster than any other region is underpinned by the extraordinary riches accumulated by the region’s Sovereign Wealth Funds.

Jordan cleans airBetween 2015-2020, Jordan grew the share of wind and solar in its electricity mix from 1% to 21%. Today, 21% of Jordan’s electricity grid is powered by solar and wind, and the country aims to reach 31% by 2030. As a result, it releases the lowest levels of CO2 emissions per capita in the Middle East (2.35 tonnes in 2021). |

These government-owned investment funds collectively hold $3.7tn in assets, more than India’s annual GDP. Just seven funds in the Arabian Gulf hold about 40% of the world’s SWF assets. And there are signs they are becoming increasingly open to investing in renewables. For example, Gulf-based SWF has bought a 50% stake in the world’s biggest private offshore wind energy developer, Germany’s Skybourne Renewables, for USD 2.5 billion, while the Abu Dhabi Investment Authority has bought a stake in Climate Technologies for $2.4bn. Meanwhile two companies owned by SWFs Masdar and ACWA Power have built around 5 GW of large-scale solar and wind projects. Given the financial muscle of SWFs, this is just the beginning.